- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

How Investors May Respond To Cabot (CBT) Missing Q4 Estimates And Flagging Mixed 2026 Outlook

- Cabot recently reported that its Q4 fiscal 2025 earnings and sales declined from a year earlier and fell short of analyst estimates, reflecting softer demand conditions.

- The company also signaled that fiscal 2026 may remain challenging for its Reinforcement Materials business, even as it expects profit growth in Performance Chemicals led by Battery Materials and other growth areas.

- We’ll now examine how weaker Reinforcement Materials trends but improving Performance Chemicals prospects shape Cabot’s investment narrative.

Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

What Is Cabot's Investment Narrative?

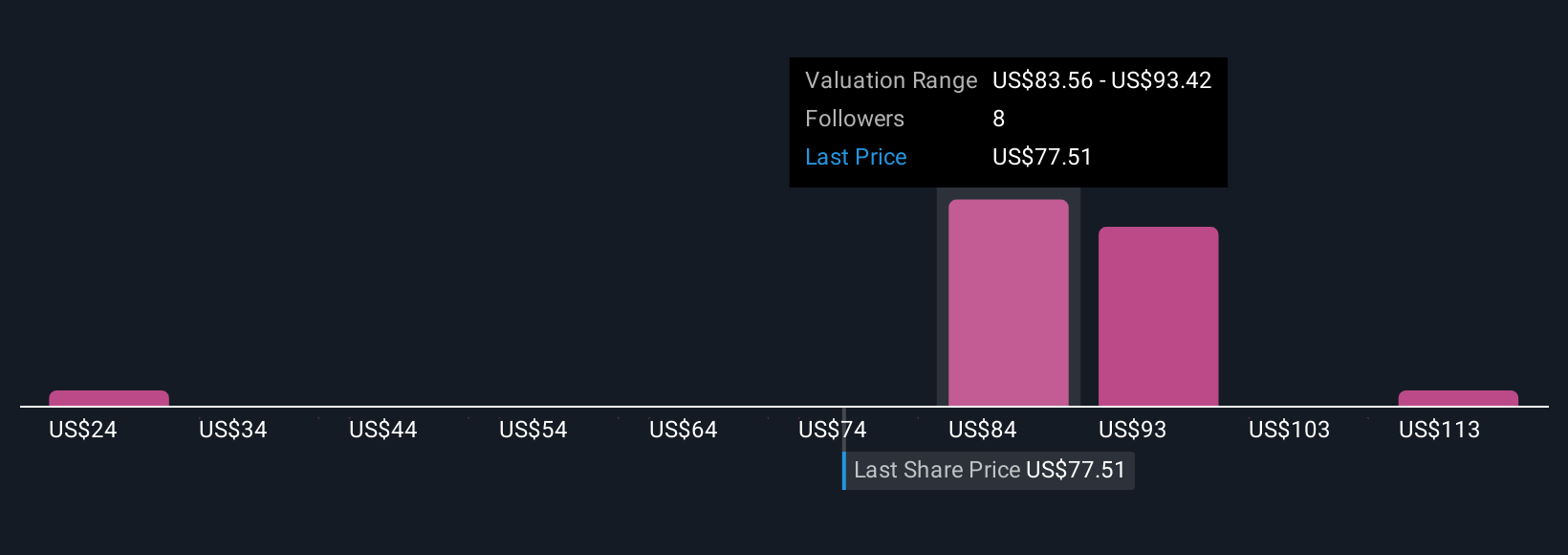

To own Cabot today, you have to believe that the company can use its high-return, cash-generating base to pivot from a pressured Reinforcement Materials business toward higher-margin Performance Chemicals, particularly Battery Materials, without eroding its financial footing. The latest Q4 miss and cautious fiscal 2026 outlook make that transition risk feel more immediate, especially after a steep share price pullback despite still-solid returns on equity and ongoing buybacks and dividends. In the near term, sentiment is likely to be driven by any signs that the new Reinforcement Materials leadership can stabilize volumes and pricing, while Performance Chemicals delivers on the profit growth Cabot is pointing to. This news effectively shifts the balance of catalysts and risks closer to execution rather than simple end-market recovery.

However, investors should be aware of how sustained Reinforcement Materials weakness could strain that transition story. Cabot's shares have been on the rise but are still potentially undervalued by 20%. Find out what it's worth.Exploring Other Perspectives

Explore 5 other fair value estimates on Cabot - why the stock might be worth less than half the current price!

Build Your Own Cabot Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Cabot research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Cabot research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Cabot's overall financial health at a glance.

Seeking Other Investments?

Our top stock finds are flying under the radar-for now. Get in early:

- Find companies with promising cash flow potential yet trading below their fair value.

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com