- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Why Agios Pharmaceuticals (AGIO) Is Down 7.1% After Phase 3 Sickle Cell Win With Mitapivat

- In November 2025, Agios Pharmaceuticals reported positive topline data from its global Phase 3 RISE UP trial, showing that mitapivat achieved a statistically significant improvement in hemoglobin response versus placebo over 52 weeks in adults and adolescents with sickle cell disease.

- An unusually high proportion of participants completed the blinded phase and almost all moved into the long-term open-label extension, underscoring strong patient retention and sustained interest in mitapivat’s potential benefits.

- We’ll now examine how this Phase 3 success in sickle cell disease, particularly the robust hemoglobin response, reshapes Agios Pharmaceuticals’ investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 24 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Agios Pharmaceuticals Investment Narrative Recap

To own Agios, you need to believe mitapivat (PYRUKYND) can grow beyond its rare disease niche and eventually scale revenues faster than expenses. The strong Phase 3 RISE UP data in sickle cell disease directly reinforces the key growth catalyst around new indications, but it does not remove the near term risk that high R&D and SG&A spend will keep the business loss making for some time.

Among recent announcements, the FDA’s December 7, 2025 PDUFA date for PYRUKYND in thalassemia looks especially important beside the RISE UP readout, since together they frame mitapivat’s near term label expansion potential while also spotlighting the emerging safety focus around hepatocellular injury and the requested REMS program.

Yet even with this clinical momentum, investors should be aware that...

Read the full narrative on Agios Pharmaceuticals (it's free!)

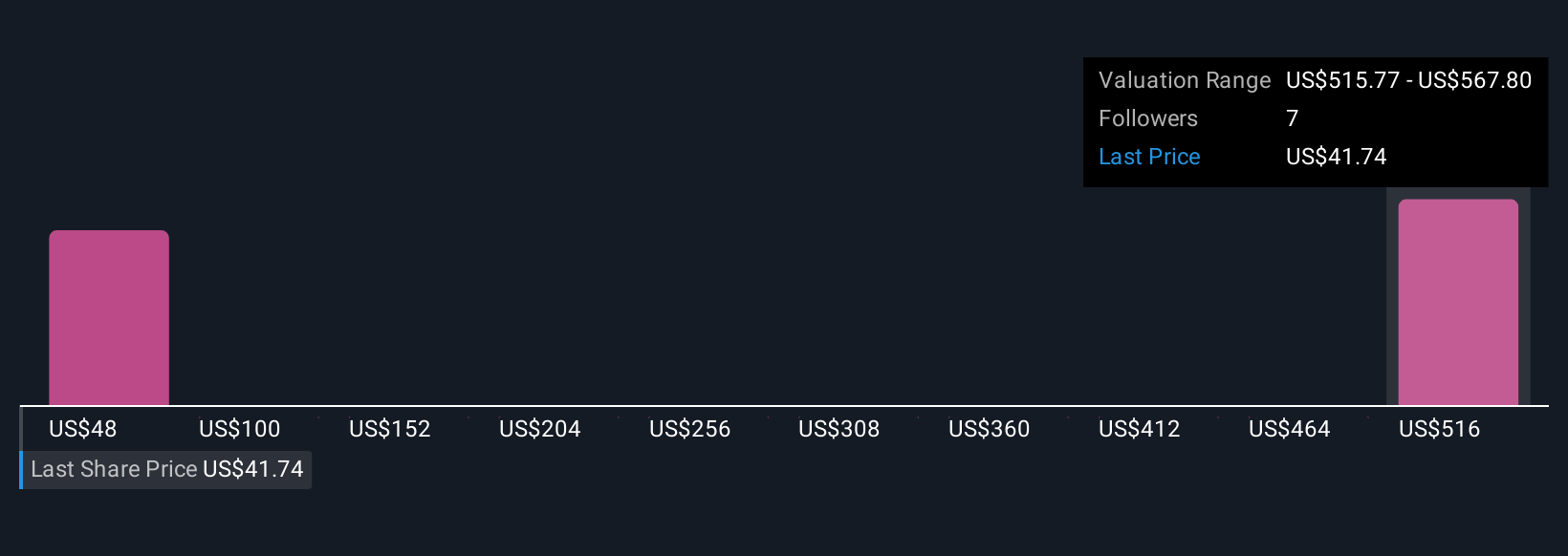

Agios Pharmaceuticals' narrative projects $416.9 million revenue and $67.0 million earnings by 2028.

Uncover how Agios Pharmaceuticals' forecasts yield a $42.33 fair value, a 57% upside to its current price.

Exploring Other Perspectives

Two fair value estimates from the Simply Wall St Community span a wide range, from about US$42 to nearly US$350 per share, underscoring how differently people view Agios’ prospects. Against that backdrop, the new sickle cell Phase 3 success and upcoming thalassemia approval decision could be pivotal for how sustainable the company’s currently loss making model proves to be over time.

Explore 2 other fair value estimates on Agios Pharmaceuticals - why the stock might be worth just $42.33!

Build Your Own Agios Pharmaceuticals Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Agios Pharmaceuticals research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Agios Pharmaceuticals research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Agios Pharmaceuticals' overall financial health at a glance.

Ready For A Different Approach?

Our top stock finds are flying under the radar-for now. Get in early:

- Rare earth metals are the new gold rush. Find out which 36 stocks are leading the charge.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've found 14 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com