- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Will Tasmea’s (ASX:TEA) Equity Raise Reshape Its Expansion Ambitions?

- Tasmea Limited has announced a follow-on equity offering of A$27.5 million through the direct listing of 5,000,000 ordinary shares at A$5.50 per share.

- This capital raising initiative follows Tasmea's recent investor briefing regarding its WorkPac acquisition, suggesting further plans for business expansion or strategic investments.

- With Tasmea’s substantial new equity offering in focus, we’ll examine how fresh capital could influence its broader investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

What Is Tasmea's Investment Narrative?

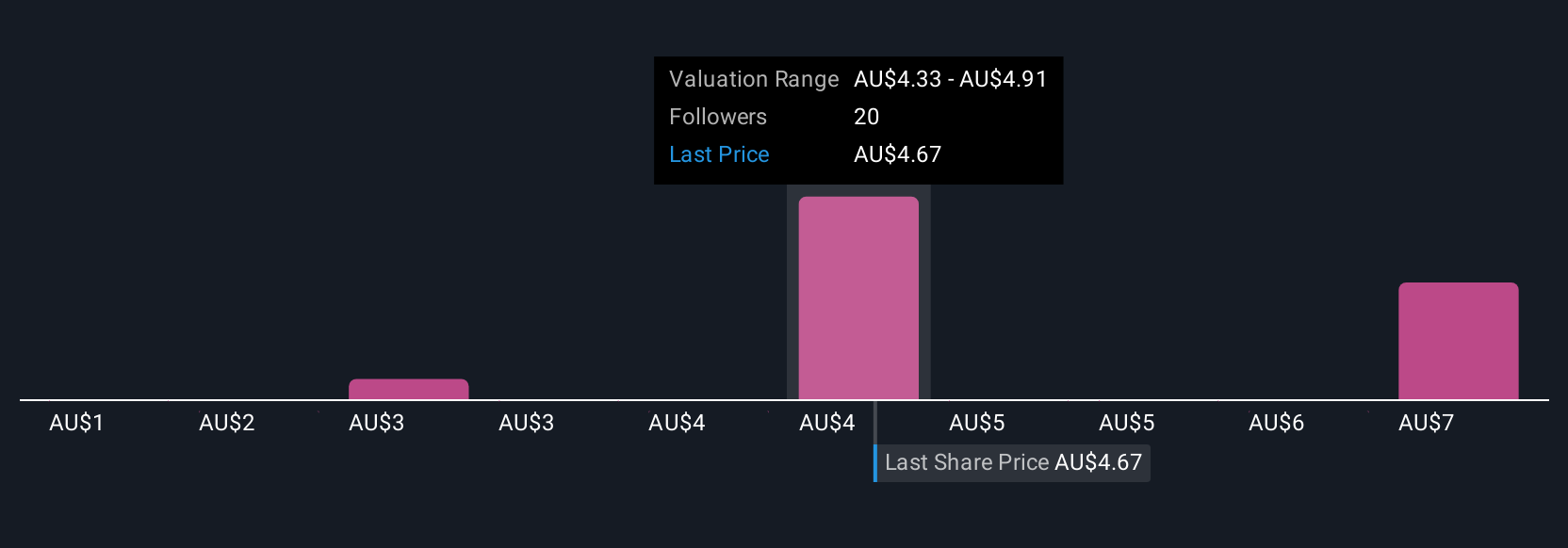

If you’re looking at Tasmea as a shareholder, the belief often centers on capturing value from the group’s ambitious growth strategy, disciplined financial management, and strong recent profit momentum. The fresh A$27.5 million equity offer, announced just after the company’s WorkPac acquisition update, could be a meaningful short-term catalyst for expanded deal-making or organic investment, particularly with prior raises helping the company accelerate both revenue and earnings growth this past year. However, this new capital can also bring increased scrutiny to execution risk, especially as Tasmea’s price has recently pulled back and the business is already trading near consensus price targets. While prior analysis emphasized earnings acceleration and strong returns on equity, the capital raising shifts the spotlight: investor attention will likely turn toward post-acquisition integration, potential dilution, and Tasmea’s ability to maintain attractive dividends while pursuing expansion. How management spends this extra capital, and the pace at which value is created from new assets, now feel like the defining variables for near-term returns.

But, if integration issues slow down the benefits from recent deals, investors could see impacts sooner than expected. Despite retreating, Tasmea's shares might still be trading 31% above their fair value. Discover the potential downside here.Exploring Other Perspectives

Explore 10 other fair value estimates on Tasmea - why the stock might be worth as much as 61% more than the current price!

Build Your Own Tasmea Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Tasmea research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Tasmea research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Tasmea's overall financial health at a glance.

No Opportunity In Tasmea?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com